By proceeding, I confirm that I am a financial professional (e.g., registered investment adviser, broker-dealer representative, or other qualified investment professional) and that I am accessing this content solely for informational and operational purposes. I understand that this material is intended for investment professionals only and is not directed to or intended for retail investors.

When Semi-Liquid Becomes Semi-Accessible: Understanding the Liquidity Mismatch in Private Debt

June 1, 2026

Steve Kirschner, CAIA®

Senior VP – National Institutions

Private debt has become a staple in advisor conversations. The pitch is familiar: higher yields, less volatility, low correlation to public markets. For many clients, those attributes are genuinely appealing. But over the past year, a different conversation has been unfolding. It centers on a structural problem inside the most popular evergreen private debt vehicles, and it has real implications for how advisors should think about liquidity.

The core issue is straightforward. Most evergreen private debt funds, particularly the large middle market direct lending vehicles that have dominated retail distribution, hold loans with stated maturities of three to five years and effective lives that often extend even longer. Yet these same funds often offer investors quarterly redemption windows, usually capped at 5 percent of NAV per quarter or 20 percent annually.

That structure works smoothly when capital comes in faster than it is going out. New subscriptions fund the trickle of redemptions, the underlying portfolio doesn’t need to change, and everyone is satisfied. The moment net flows reverse; the math gets uncomfortable. A fund holding multi-year senior secured loans may have difficulty liquidating those positions on a quarterly basis. The loans don’t trade in any deep secondary market, the borrowers aren’t expecting to be refinanced on the fund’s redemption schedule, and selling at par may not be an option when other investors are heading for the same exit at the same time.

This is the duration mismatch at the heart of issues being experienced within private evergreen vehicles today. It isn’t a flaw in any single manager’s strategy. It is a structural consequence of placing three-to-five-year loans inside a quarterly liquidity wrapper.

In late 2025 and early 2026, several of the largest non-traded private debt vehicles began limiting redemptions as withdrawal requests increased above the quarterly caps and importantly climbed faster than new capital was coming in. The dynamics weren’t complicated. When outflows outpace inflows and the underlying loans can’t be liquidated easily, something has to give. Investors who thought they had quarterly liquidity found themselves receiving less than they requested and potentially waiting for several quarters to be made whole.

This isn’t a crisis in the traditional sense. The loans themselves haven’t necessarily gone bad. But it does reveal a meaningful gap between how some of these products are marketed and how they actually function under pressure. Quarterly liquidity windows that exist on paper can close quickly in practice, particularly if many investors are trying to exit at the same time.

For advisors, this matters a great deal. Clients don’t always internalize the difference between “periodic liquidity” and “real liquidity.” When a client needs funds for a business situation, a tax payment, or simply because they have changed their mind, the response “you may have to wait” is a difficult conversation.

The duration of the underlying loans is critical to maintaining the availability of liquidity.

This is the question advisors should be asking when evaluating any private market allocation that offers quarterly liquidity. What is the actual weighted average life of the investments in the portfolio? If a fund offers quarterly redemptions but holds assets that turn over every four or five years, the fund is implicitly relying on continuous net inflows to honor those potential redemptions. That works until it doesn’t.

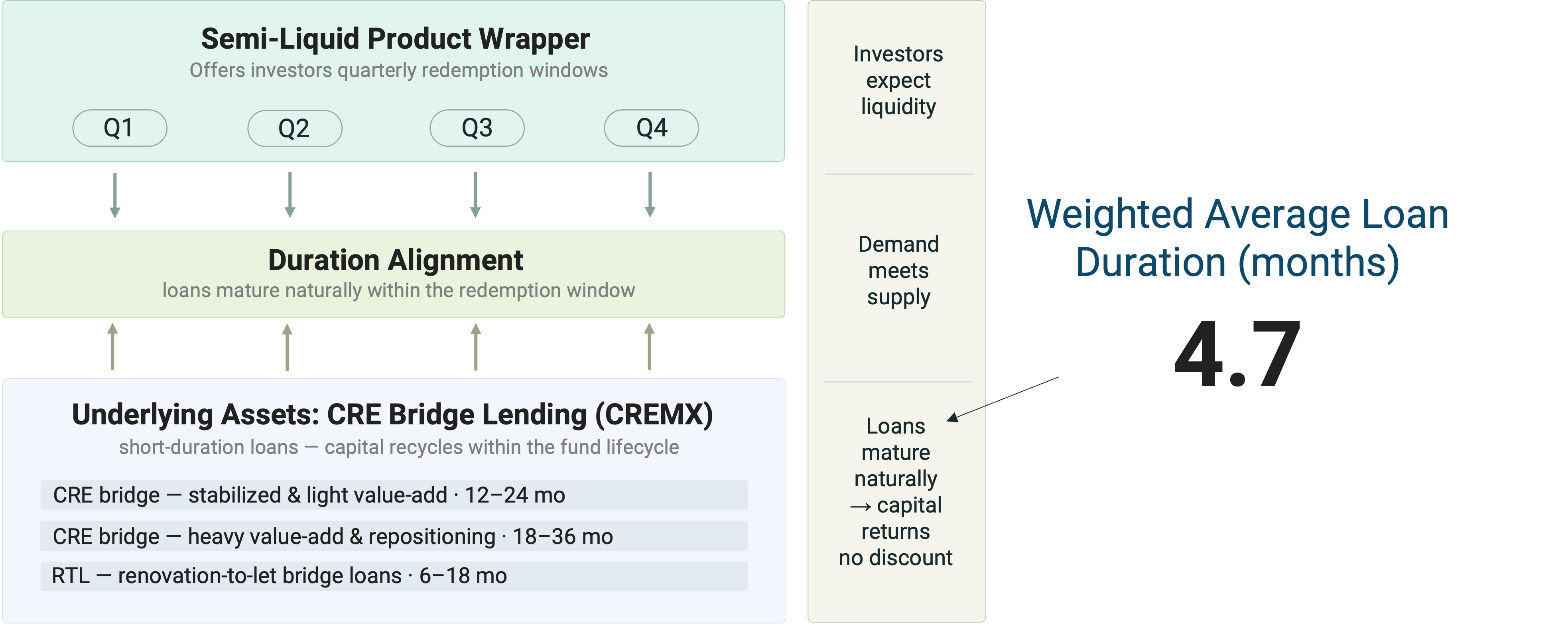

A more durable approach is to match the liquidity profile required by the investment vehicle with the natural liquidity of the underlying loans. In practice, a portfolio built around shorter duration debt, where loans are maturing inside the same window that investors might request redemptions, generates its own liquidity from the bottom up. The fund doesn’t need to find a buyer for a five-year loan to meet a quarterly redemption. Rather, liquidity within the portfolio is simply aligned with redemption schedule of the fund.

This is the structural advantage CREMX offers in the quarterly liquidity context. Rather than placing multi-year middle market loans inside a quarterly redemption wrapper and hoping that inflows hold up, CREMX is built around short duration commercial real estate loans whose natural turnover align with the redemption schedule the fund offers. The duration mismatch that has tripped up larger evergreen middle market lending funds simply isn’t present in the same way.

For advisors who want exposure to private debt but also want the quarterly liquidity to naturally flow from the portfolio, that distinction is worth taking seriously.