By proceeding, I confirm that I am a financial professional (e.g., registered investment adviser, broker-dealer representative, or other qualified investment professional) and that I am accessing this content solely for informational and operational purposes. I understand that this material is intended for investment professionals only and is not directed to or intended for retail investors.

The Four Dimensions of Liquidity

July 20, 2026

Steve Kirschner, CAIA®

Senior VP – National Institutions

In the first post in this series, we looked at a structural problem hiding inside the most popular evergreen private credit vehicles: loans with three-to-five-year maturities placed inside a quarterly redemption wrapper, and what happens to that arrangement when net flows reverse. The takeaway was that quarterly liquidity windows which exist on paper can narrow, or close, in practice.

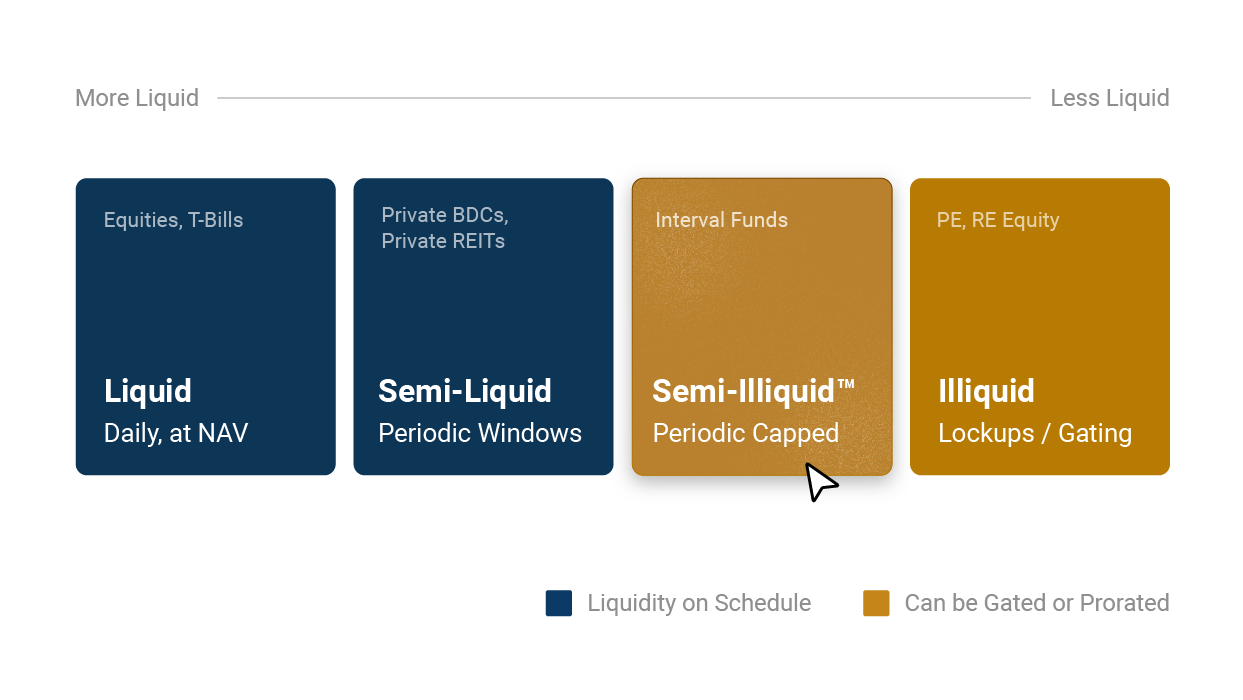

That post raised a question worth answering directly. If the liquidity a product advertises is not always the liquidity an investor receives, how should advisors think about liquidity in the first place? The vocabulary is part of the problem. We tend to sort investments into two buckets, liquid and illiquid, when the reality is a spectrum. We find it more useful to think in terms of four dimensions of liquidity: liquid, semi-liquid, semi-illiquid™1, and illiquid. The distinctions among them are not academic. They determine what an investor can actually do with their capital when they need it.

Liquid. These are public securities with tickers and active daily volume: listed stocks, exchange-traded funds, and daily-priced mutual funds. There is a continuous, observable market. An investor can sell today at a price set by the market and expect cash to settle within days. Liquidity here is a feature of the asset itself, not a promise layered on by a fund structure. This is the benchmark against which every other dimension should be measured.

Illiquid. At the far end sit drawdown vehicles: private equity, venture, and credit partnerships with capital commitments, lockups, and defined investment and harvest periods. An investor commits capital, it is called over time, and it is returned over the life of the fund as the underlying assets are realized. There is no periodic redemption right and no expectation of one. The defining characteristic of illiquid investments is that everyone understands the terms going in. The illiquidity is explicit, priced, and accepted.

Semi-Liquid. The genuine middle ground takes two forms. The first is a public security that trades but lacks active daily volume, where a market exists but is thin enough that selling a meaningful position can move the price. The second is a vehicle that offers periodic but real liquidity, such as a hedge fund that allows investors to redeem the full value of their interest once a year. The common thread is that when the liquidity window opens, the investor receives what they ask for. Access may be infrequent, but it is dependable.

Semi-Illiquid™. This is the dimension that causes the most confusion, because it is so often labeled semi-liquid. We use semi-illiquid™ to describe private asset funds that are continuously offered and provide a prescribed amount of liquidity to shareholders periodically. The reason for the distinction is structural: the product takes a fundamentally illiquid private asset and layers a small, capped, periodic liquidity feature on top of it. An investor may well be able to redeem their entire position in a given quarter. It is equally possible that they receive only a portion of what they requested if total redemption requests across all shareholders exceed the fund’s quarterly repurchase cap — commonly set at around 5 percent of the fund’s outstanding shares — and the fund has to prorate. The cap applies to the fund’s aggregate repurchase, not to each investor’s own position; an investor is paid a pro-rata share of what they asked for, not a flat 5 percent of their investment.

This is where most evergreen private credit funds and interval funds actually live, and it is the dimension the first post was really describing. Many products marketed as semi-liquid are, on close inspection, semi-illiquid™: the liquidity is conditional, capped, and dependent on the behavior of other investors in the same fund. That is not a criticism of the structure. It is simply a more honest description of what the structure can and cannot do.

Which points to the distinction underneath all four dimensions: the liquidity of the wrapper and the liquidity of the underlying assets are not the same thing. A fund structure can promise periodic liquidity, but only the underlying assets can actually deliver it. A quarterly redemption right is a feature of the legal structure. The ability to honor that right in full, in every market, comes from holding assets that mature or trade on a timeline compatible with the redemption schedule. When the two are aligned, a product behaves much closer to genuinely semi-liquid. When they are not, the structure is writing a check that only continuous net inflows can cash.

Proration is not gating

These two events look similar from a client’s seat — “I asked for my money and didn’t get all of it” — but they are fundamentally different, and the difference matters. Proration is the fund honoring exactly what it promised. An interval fund that offers to repurchase 5 percent of NAV per quarter and receives requests for 10 percent of the total shares will pay everyone half of what they asked for. The fund offered 5 percent from the outset and is delivering 5 percent. Nothing has been restricted or limited; the cap is doing precisely what it was designed to do when demand runs ahead of it. Gating is a discretionary suspension or restriction of redemptions, typically invoked when a fund holds distressed assets, or assets the adviser believes are worth more than they could currently fetch in an arm’s-length sale. Rather than dump those holdings at distressed prices to the detriment of remaining shareholders, the adviser closes the door to protect the pool’s capital.

The Third Avenue Focused Credit Fund (TFCIX) is the canonical example. In December 2015, with redemptions overwhelming a portfolio of illiquid, deep-value high-yield debt, Third Avenue Management halted redemptions and moved the fund into a liquidating trust, stating that the bids available for many positions would have unfairly disadvantaged shareholders. That is gating. Proration is the system working as designed; gating is the adviser stepping in because the alternative is worse.

Holding these distinctions in mind changes the questions an advisor asks. Knowing which of the four dimensions a product occupies tells you what to expect from it under stress, before stress arrives. A liquid fund returns capital on demand. A semi-liquid one returns it dependably when its window opens. A semi-illiquid™ one offers a capped, periodic right that can shrink through proration in the ordinary course, and, in a more difficult scenario, can be suspended through gating. An illiquid one never offered redemptions at all. None of these is inherently good or bad. The problem arises only when a product sold as one dimension behaves like another.

This is why the principle from the first post matters as much as the vocabulary. The closer the natural liquidity of the underlying assets sits to the liquidity the wrapper offers, the closer a product moves toward genuine semi-liquidity, and the smaller the gap between what is marketed and what is delivered. A portfolio of short-duration loans that mature inside the same window in which investors might request redemptions generates its own liquidity from the bottom up, rather than relying on the next investor’s subscription to fund the last investor’s exit. That is the design idea behind a vehicle like CREMX, and it is the thread connecting both posts: structure can promise liquidity, but only the underlying assets can produce it.

1. Semi-IlliquidTM is a proprietary Redwood Investment Management framework used to describe investment vehicles that provide periodic liquidity subject to repurchase caps, proration, or other structural limitations. It is not an industry-standard classification.

Interested in Learning More?

Have questions about CREMX, interval funds, or portfolio construction? Our team is here to help.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.